Table of Contents

The Acorn

When I started out doing the job at Morningstar (MORN), on Feb. 15, 1988, the mood was subdued. Reeling from stocks’ 22% loss on Black Monday (which stays the biggest single-working day drop in U.S. inventory-sector historical past), traders feared the fantastic instances have been around. Each equity and bond costs had relished a splendid 5-calendar year run from 1982 via mid-1987. Now, it seemed, normalcy would return.

Alternatively, the rocket ship arrived. The inventory current market went just about straight up, year after calendar year, with inflation and fascination rates heading down. The fund organization followed suit. Historically anything of an financial commitment backwater–moving into the 1980s, the industry’s yearly revenues were being less than $500 million–mutual money hit the mainstream. It was all pretty thrilling. I was specially happy for the reason that soon soon after joining the business, I experienced ignored the skeptics and put all the things I experienced (not a great deal) into a thoroughly invested inventory fund.

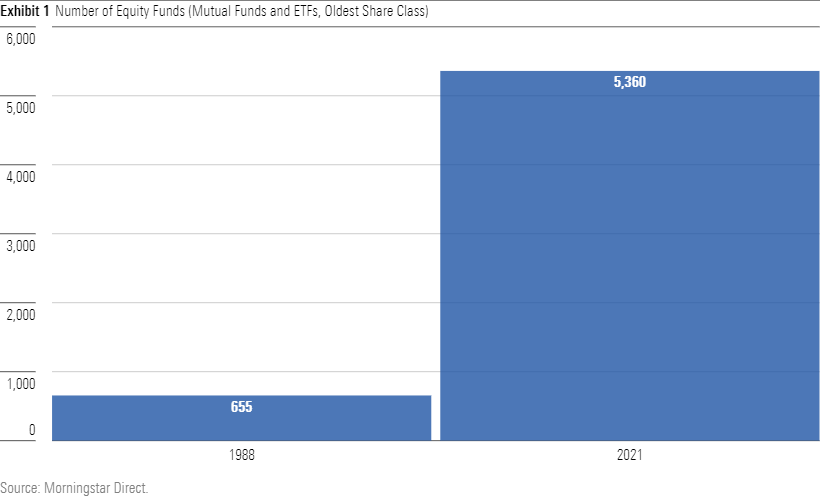

In the early a long time, Morningstar analysts wrote reports on every single present inventory fund, together with the $5 million Valley Forge Fund, operated by a partner-and-spouse crew. (“Bernie can not occur to the mobile phone now. Can I have him phone you again, immediately after he finishes mowing the garden?”) Attempting the identical feat today would demand a much larger sized exploration team. Like exchange-traded resources, the equity fund depend has octupled.

Revenue, Dollars, Funds

While spectacular, the boost in the range of funds has enormously lagged the surge in fund assets. In 1988, the largest mutual fund was Franklin U.S. Authorities Securities (FKFSX), which finished the yr with $11.7 billion. (Shut guiding was one more bond fund, Dean Witter U.S. Govt Securities Belief (USGAX), which has due to the fact been renamed right after its current owner as Morgan Stanley U.S. Authorities Securities.) Today, 348 mutual resources and 124 ETFs exceed that figure.

The subsequent chart, contrasting mutual-fund property in 1988 with all those for 1) mutual resources and 2) ETFs in 2021, efficiently conveys the tale. When I initially arrived at perform, the industry’s progress experienced only just begun.

Sure, people quantities are not inflation-adjusted, but performing so would simply bump the 1988 determine to $1 trillion. That original year would still scarcely sign up on the chart.

The Index Revolution

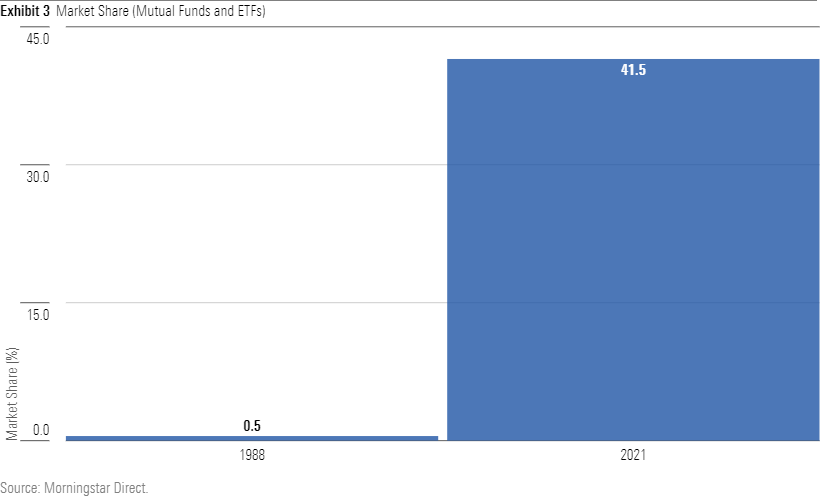

Other than spectacular growth, the other exceptional fund development has been the triumph of indexing. In 1988, 3 index cash existed: 1) Vanguard 500 Index (VFINX), 2) DFA U.S. Micro Cap (DFSCX), and 3) a manufacturer-new entrant from Fidelity that was eventually merged into the company’s present providing Fidelity 500 Index (FXAIX). (Even that list is suspect, as DFA now states that its resources are actively managed. Even so, as it known as DFA U.S. Micro Cap an index fund at the time, that is the place I have placed it.) In combination, those people money held $2 billion, creating for a sector share of somewhat below .5%.

Currently, index money account for far more than fifty percent of fairness fund property and just more than 40% of the total marketplace. That percentage surpasses my seemingly rash prediction from the early 1990s that indexers could possibly inevitably control 30% of the fund small business, which I experienced flippantly made available to a Funds reporter. That grew to become the story’s key quotation. Lively administrators were being, shall we say, unamused.

The Price tag Is Correct

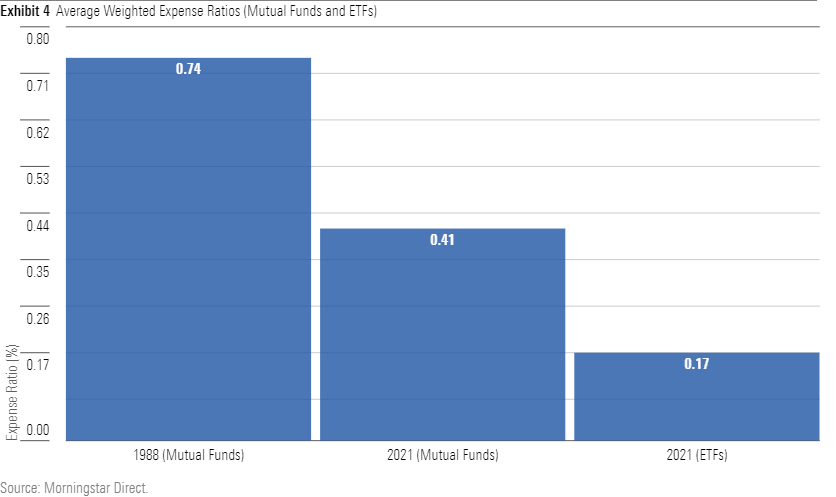

Accompanying index funds’ advance has been higher awareness of fund expenditures. Back again in the day, buyers who emphasised fund expenditures ended up seen as cranks. Existence was as well brief to fear about a couple of basis details. In 1993, for example, the five leading-marketing mutual funds carried normal an regular expenditure ratio of 1.09%. When effectiveness was robust, cost was not a barrier.

That angle has sharply adjusted, as mirrored not only in today’s most effective-vendor lists– which are dominated by index resources–but also in the industry’s ordinary greenback-weighted cost ratio, which reflects where traders now maintain their monies. That has dropped sharply, from .74% for all inventory, bond, and allocation resources in 1988, to .41% for mutual money nowadays, and a piddling .17% for ETFs. Whilst equally direct buyers and economical advisors when downplayed the importance of price when analyzing cash, they now location cost ratios front and center.

Admittedly, the all-in expenditures for fund buyers haven’t dropped as dramatically as the numbers would appear to be to show. Today’s economical advisors are compensated otherwise. While they after ended up almost exclusively paid out by fund firms, which embedded income charges into their products and solutions, advisors now typically cost asset-based mostly service fees. So, quite a few fund buyers shell out far more than the figures suggest. On the other hand, their passions now align with their advisors’. For every single social gathering, the more cost-effective a fund, the much better.

In fact, now that they have turn into low cost purchasers, economic advisors favor employing institutional shares. Following all, why should their purchasers shell out more, when advisors can use their insider standing to prepare superior specials? That the market has grow to be so substantial, with popular advisors putting tens of millions of dollars with a single fund team, has strengthened their negotiating electric power. As a outcome, fund organizations have progressively produced their institutional shares available to all.

Glory Times

The fund industry’s boom greatly benefited Morningstar. My job has consequently been blessed. Whilst most people from my generation have not savored related doing the job problems, all were granted the exact same fantastic financial investment chance. The fund company was not alone in outstripping expectations. So, much too, did inventory and bond performances, which very easily outpaced inflation. These who held bonds profited. Individuals who held equities fared greater however. A lot of turned wealthier than they at any time would have imagined. The chart below offers the facts, for the 33.5 decades that have handed due to the fact Aug. 1, 1988.

Whether the future era will take pleasure in related expense results continues to be to be noticed. The consensus is if not. Most institutional scientists anticipate the just after-inflation returns for equally equities and bonds more than the up coming one particular third of a century to fall significantly quick of what the most-current third sent. That may perhaps effectively happen I really don’t argue with the forecasters. Nonetheless, it is value remembering that when my particular journey commenced, the wise aged heads sounded the very same be aware. As Yoda would say, mistaken they had been.

Joyful vacations, and may your fortunes be as generous as mine have been.

Editor’s Observe: The reference immediately after Exhibit 2 to the 1988 determine was corrected to trillion, not billion.

John Rekenthaler ([email protected]) has been researching the fund sector due to the fact 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s investment study department. John is rapid to position out that even though Morningstar typically agrees with the sights of the Rekenthaler Report, his views are his possess.

More Stories

York County tends to make a $45 million financial commitment to address opioid epidemic

Axis Genuine Estate Expense Have faith in (KLSE:AXREIT) is favoured by institutional house owners who maintain 52% of the firm

Bonds Have Been Terrible Investments. It’s a Excellent Time to Obtain.